Money cant buy happiness, but it can sure put a smile on your face

Any advise on future savings if you make 60.000 a year ( 30.000 after tax)? Besides earning more money

On 7/31/2017 at 1:11 am, Gregor Sonin said... Any advise on future savings if you make 60.000 a year ( 30.000 after tax)? Besides earning more money

I decided to pare back most of my life insurance as I am 56 and have accumulated enough of a net worth that it was no longer necessary.

I dropped a bunch of term, but left in place some term to cover my building SBA loan as required. The rest was whole life which had enough of a dividend to let the dividend cover the premium.

What you find out right away, is that this major selling point 30 yrs ago, was a bit of a sham. Once the premium is paid by the dividend, the death benefit of the policy plummets. Also, if I take a loan from the cash value, I pay 8%. If it let it ride, the borrowed amount comes out of the death benefit and there are tax consequences.

I also dropped some disability that had the highest cost to benefit ratio.

At the end of this, my NWML agent, who had been a patient for 20+ years, bailed out of my practice. I had taken the gravy off of his train, and he did not like it one bit.

Whole life is truly a scam. We are all now or eventual high net worth individuals who can shit can life insurance at some time in our 50's. There is no need for permanent life insurance.

Hi All,

I wrote up a new REAL last will and testament a few years ago, all bases covered. And like you all sold my whole, B.S. life policies. We actually did have enough equity to cover my husband's policy and majority of mine. One bad advice my dear dad gave me was this horrible insurance. Sweet talking advisor, I called every year when I had to pay the premium, got sweet talked by secretary. My advisor wasn't there anymore, wouldn't put me through to the guy in charge. I finally got fed up with the price of the whole life insurance. Bad decision, hope this post helps others to stay clear.

Carrie

So the Dow just crossed the 22000 mark. Who here would have thought that we would be up 3.4x since the market crashed in 2008? How many of you remember the doom and gloom predicted by the pundits on TV? Now Im sure many of us thought the world was ending as our insurance salesmen crawled out of the woodwork to sell us "guaranteed" returns because you know, hey, this time its different. We will never see the historical returns that we have seen in the past and that you have to protect your future. Well, its not different. Its the same. Invest in the market long term and you come out ahead. The last 10 years prove it.

Lets say we panicked in 2008 and put 100k worth of premiums in a whole life type policy because you fear the future is never going to be the same and the historical returns of 11.4% aren't guaranteed if you just do regular investing. So what the hell, you buy into the sales pitch where the agent says Ill guarantee you 6% with my whole life policy. So you take whatever little cash you had sitting around and instead of buying more at the market lows of 6594.44 on March 5, 2009 you instead take out a whole life policy with the promise of a guaranteed return.

Fast forward 9 years, today that 100k would be worth a hypothetical 168,947.90 with those 6.0% guaranteed returns. I say hypothetical because that isn't the actual cash value. See Brian's post above- there are fees, taxes, surrender charges all to consider. But hey- you have insurance and you have guaranteed returns, likely far less than the 168k at a 6% return for 9 years but its something.

Now had you ignored the hype and had you ignored the sales pitch and had you taken emotion out of your investments, and realized that its not different this time, its the same as it always has been. Markets have corrections, markets have ups and downs. But in the long run, the trend is up. So instead of investing with emotion and fear that 6594.44 wasn't going to be the bottom but the stock market was going to -zero- you realized that what goes down, must come up and you invested 100k and bought into the broad market. Since the crash in 2008, from 2007-2016, the market has returned 8.6%, less than the 11.4% average returns since the 20s but that is taking a 30% or so loss in the market in 2008. That 100k 9 years later would be worth 210,992.77.

And guess what- no surrender charges like whole life, no commissions like whole life, no penalties like whole life. If you figure in the massive run up that we have had in 2017 and add one more year to the returns, that 210k comes closer to 236k. All this through probably the worst economic downturn we have seen in our lifetime and likely wont ever see anything like this again. How do I know? I dont, but I do know that if we crash again, Ill buy more and stay the course as my investment outlook is long term. im so confident on this that Im betting my life savings by staying invested.

Stay the course folks, and dont get caught up in fancy alternative investments. If you need insurance, buy term until your net worth reaches a point where you dont need insurance anymore. You should have enough insurance that if you were to pass unexpectedly, you leave enough money to your heirs to allow them to continue their lifestyle. If you have enough saved up, cancel the insurance. But if someone is selling you something that appears too good to be true- its probably is.

At the time of that crash I was given the book "How to become your own banker" by a "financial adviser" peddling this whole life insurance idea. Thank god it sounded too good to be true so I passed.

The biggest mistake I made though was not to buy CITI or AIG stocks when they were $1 each or 50 Cents each. Big Brother will never let these type of companies or the stock market crash long-term...Unless of course we have an alien invasion that takes out Big Brother.

Farhad

On 8/2/2017 at 11:51 am, Farhad Boltchi said...At the time of that crash I was given the book "How to become your own banker" by a "financial adviser" peddling this whole life insurance idea. Thank god it sounded too good to be true so I passed.

The biggest mistake I made though was not to buy CITI or AIG stocks when they were $1 each or 50 Cents each. Big Brother will never let these type of companies or the stock market crash long-term...Unless of course we have an orange-skinned alien invasion that takes out Big Brother.

Farhad

On 8/2/2017 at 11:51 am, Farhad Boltchi said...At the time of that crash I was given the book "How to become your own banker" by a "financial adviser" peddling this whole life insurance idea. Thank god it sounded too good to be true so I passed.

The biggest mistake I made though was not to buy CITI or AIG stocks when they were $1 each or 50 Cents each. Big Brother will never let these type of companies or the stock market crash long-term...Unless of course we have an alien invasion that takes out Big Brother.

Farhad

I remember staring at AIG. that was a missed opportunity for sure.

I agree with joel

no argument cleverly live assurance packages are pants but advising to pay an advisor 1% of your fund is not much better.

depending on your risk tolerance get a low cost world market etf and have min risk for max long term benefit.

less than 2% of fund managers beat the index

don't pay them 1% which is a fortune over time

On 8/3/2017 at 10:41 pm, Patrick Oconnor said... I agree with joel

no argument cleverly live assurance packages are pants but advising to pay an advisor 1% of your fund is not much better.

depending on your risk tolerance get a low cost world market etf and have min risk for max long term benefit.

less than 2% of fund managers beat the index

don't pay them 1% which is a fortune over time

This is certainly a good debate to have Patrick but I think you are misunderstanding what a financial advisor does. They are there to provide guidance on finances, taxes, estate planning and much more. Certainly you can do it your self. I choose not to as I feel the money Ive paid has been well worth it as my returns have been at or above the general index even after considering the fees Ive paid.

At this point in my career I choose to get professional guidance. Others may find that investment not necessary. Its ok. This doesnt change however the basic premise of the blog- invest wisely and dont buy investment vehicles that generate a massive commission for the agent thereby sucking into your returns.

I continue to be amazed at the number of people that continue to use or recommend insurance as an investment. This is one of the most expensive ways you can invest for your future. Lets not even get into the fact that its also an expensive way to insure your family.

I know Im beating a dead horse here but i feel I need to provide whatever encouragement I can to folks to invest for the long term and don't buy into sales pitches for expensive insurance policies. As I've stated before, we have close to 10,000 dentists that come to our center in Scottsdale for seminars and workshops every year. This doesn't even include all the people that are online in our various communities. I get the joy and privilege of interacting with many of the docs that come on campus for education. And too many times now I have had to sit down with a doctor who is struggling with their practice or struggling financially. It made me realize how financially illiterate many dentists and physicians are.

The constant talk on this forum espousing the benefits of insurance as an investment reinforces that view. I hate to see dentists struggle. We have an incredible profession. There is no reason that dentists should struggle. There is an opportunity to make a great living but bad investments lead to a poor financial outcome. Investing in a cash value insurance policy certainly doesn't help yet over and over again, this form of "investment" is given as an option for doctors.

I've repeatedly asked for examples of where buying a cash value makes any sense for a typical dentists and not once has anyone given a single scenario where it makes any sense to buy an expensive insurance and an expensive investment. This is not just me saying this. Go spend some time on White Coat Investor. Or spend some time listening to Dave Ramsey. These policies have high commissions which I have no issues with people making money but these high commissions eat into the return for the doctor. If I invest 500k and the commission is 15% - that's 75k that the doctor is in the hole.

This is precisely why the returns are so low for these policies. Yet these are being pushed again and again to doctors who don't know any better. The biggest reason these are promoted is because you know, we have a rough few years coming up as we are constantly being reminded. Things cant always go up we are told, so these policies are guaranteed - of course the guarantee caries a lower rate of return. Much much lower.

The crash of 2008 is used as a warning that buyer beware and one should be careful of investing in the market. You will potentially lose all your money if another crash like 2008 happens.

Lets do some math shall we and see what happens if we invest for the long term and don't let emotions get in the way of bad judgment. I've attached a link here of the S&P return since 1989 - that's the year I graduated from high school and that's the time-frame I will use to demonstrate how bad of an investment cash value life insurance like whole life is. Please know that if we use even longer periods, the rate of return from the S&P from 1926 to 2016 is 11.42% - that's taking into account all the wars, all the recessions, all the depressions, all the bad things that happened in this world. Here is the link if you want to verify the return rates that Im using.

https://ycharts.com/indicators/sandp_500_total_return_annual

So if I was to start investing in a low cost S&P index fund that has little to minimal commissions the year I graduated high school in 1989 and calculated the returns till the end of 2017, my average rate of return would be 11.67%. Wait just a minute Sameer! Didn't the market totally tank with the internet bubble around 2000 or so? And didn't it tank again with the Great Recession in 2008?

Yes. Yes it did and if you take the -22.1% return of 2000 and the -37% return of 2008, you still come out ahead at 11.67% from 1989 to 2017.

But I had no money graduating from high school so if now look at the scenario of investing from the year I graduated college in 1993 to 2017, my return rate would average 10.9%.

Ok you got me, I was still a poor student going into dental school so lets take the year I graduated dental school in 1997 and calculate the rate of return till 2017 and I get a return of 9.62%.

But Sameer, you are cherry picking the numbers. What if you started investing and saving in 2006, just a few years before the crash of 2008 and calculated the rate of return till 2017? That rate of return would be 9.78%.

And if you were really unlucky and started investing in 2008- the year we had a meltdown and the market lost 37% of its value and calculated the return till 2017 - your rate of return would still be 9.63%

On the other hand if you were lucky and graduated from school and became super disciplined and started putting money away in 2009- your average rate of return would be 14.29%.

So worst case scenario for me, in my adult life the worst Ill do by investing in the market is 9.63%. Again, knowing that close to a 100 years the market has returned 11.42% since 1926, the longer I stay in the market, the bigger the rate of return.

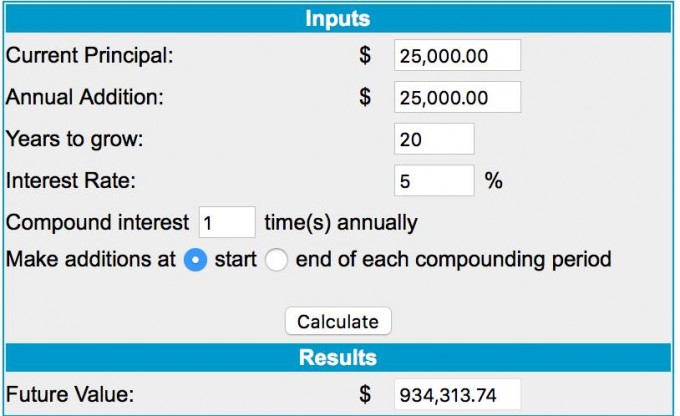

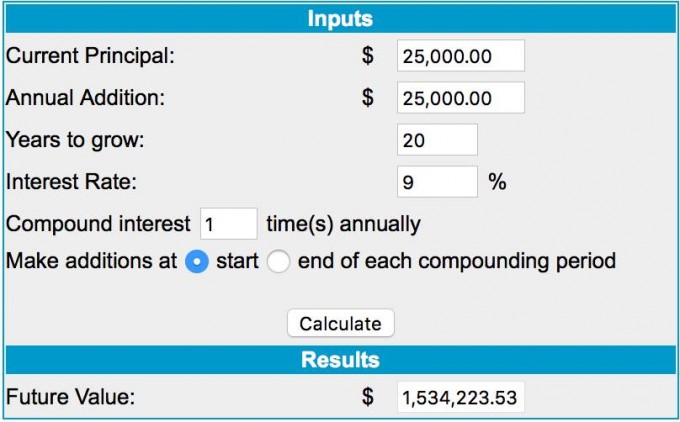

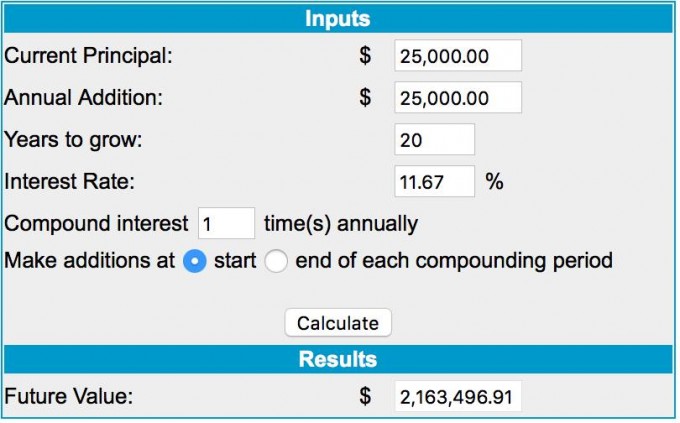

But whole life is guaranteed. Whole life is safe. Right? You can look at it that way but its expensive and a lower rate of return. If I take 25k a year and invest it for 20 years adding 25k every single year and get a 5% rate of return, I end up with a touch over 934k. If I take the exact same money but instead get a 9% rate of return, my balance is roughly 600k higher at 1.534 million. If I calculate an 11.67% rate of return, the rate of return from when I graduated high school, my balance pre tax is 2.163 million. Double, that's right DOUBLE of what you would get over the insurance policy. Yes you have to take out taxes but you still come out way way ahead.

I said it before and Ill say it again- I remain unconvinced that whole life insurance polices are a good investment. They are expensive, they are are costly and provide a poor rate of return and for the average individual, they should not be a part of your overall portfolio.

Thought I'd revive this thread into the active topics since a kind reader of this website dropped by my website recently from a post above. I created a PUBLIC post on 10/2 that read as follows--you can find it HERE at dentistmarketalert.com:

Still looking for a daily close above 2941 S&P

Published October 2, 2018 by Dr. JAs pointed out in the month-end post for subscribers, the bulls are looking for a daily close above 2941 to open the door for a bigger move upward in the future. We started the first day of the month with a big push up on the “new NAFTA” trade agreement news, only to lose ground all day and never got above, let alone close above, the magic 2941 level. I’ll be watching this week for a daily close above this level to indicate more upside on the way. If you are looking for a short position, this could be a good place to take a bite at the apple. Why? Because if you took a position in the 2930’s, once price closed above 2941, you’d exit the position and chalk it up as a loss. Nice try. If it works out, you’re in GREAT position to ride that short for a decent gain if price continues to fall. Trading 101. Hope that helps someone out there.

On 10/5/2018 at 8:57 pm, Ernie Johnson said...Thought I'd revive this thread into the active topics since a kind reader of this website dropped by my website recently from a post above. I created a PUBLIC post on 10/2 that read as follows--you can find it HERE at dentistmarketalert.com:

Still looking for a daily close above 2941 S&P

Published October 2, 2018 by Dr. JAs pointed out in the month-end post for subscribers, the bulls are looking for a daily close above 2941 to open the door for a bigger move upward in the future. We started the first day of the month with a big push up on the “new NAFTA” trade agreement news, only to lose ground all day and never got above, let alone close above, the magic 2941 level. I’ll be watching this week for a daily close above this level to indicate more upside on the way. If you are looking for a short position, this could be a good place to take a bite at the apple. Why? Because if you took a position in the 2930’s, once price closed above 2941, you’d exit the position and chalk it up as a loss. Nice try. If it works out, you’re in GREAT position to ride that short for a decent gain if price continues to fall. Trading 101. Hope that helps someone out there.

Sorry Ernie. We invest with Matson Money and follow Mark Matson's program. I do not think that anyone can consistently out guess the Market. Matson's philosophy of re-balancing provides us with consistent gains and buffers the bad times. We don't like the wild fluctuations that plague the Stock Market on a regular basis.

On 10/10/2018 at 6:14 pm, Charles LoGiudice said...Sorry Ernie. We invest with Matson Money and follow Mark Matson's program. I do not think that anyone can consistently out guess the Market. Matson's philosophy of re-balancing provides us with consistent gains and buffers the bad times. We don't like the wild fluctuations that plague the Stock Market on a regular basis.

I'm happy for you and anyone else that uses a financial advisor to help them navigate their financial future. Sam does as well, and has done nicely with them.

My reply is a simple one to explain it, but complex to back it up: the long term model I demonstrated for my fellow Mentors is simply an If/Then, rules-based investment philosophy designed specifically for the US equity portion of retirement portfolios that actually ELIMINATES "guessing" as you refer to it.

My personal belief is that MOST financial advisors do NOT have their client's maintenance of wealth as their central tenant and goal, rather it is to accumulate Assets Under Management so they can profit from the relatively small skim off those big pools of money being fed into the market via mutual funds under ANY market circumstance. Very, very few financial advisors ever tell their clients to shift their asset allocation into more conservative or safe investments when the market has delivered a pattern of behavior that is consistent with previous patterns of wealth destruction. The very best do, and I applaud them. Nobody can call the exact top or exact bottom of the stock market on a consistent basis, and that is a fool's errand. But to invest in the trend to the upside, and AVOID the trends to the downside, are the golden rule of investing (buy low, sell high). Riding them both up and down without asking "why can't I avoid this" is a sure fire way to create anxiety in my opinion. If you never SELL, how can you buy low and sell high? I personally think the entire group of investors today have been brainwashed into thinking they HAVE to ride the LARGE ups and downs since "NOBODY" can offer a solution. My website offers a solution...it is up to YOU to implement that information and take responsibility for your results. If my model says SELL and your advisor says "hang in there, it'll be fine." Are you ready for another 2000 or 2008 where 50% is lopped off your wealth? I don't know when that SELL signal is going to happen, but the model will most likely indicate when the conditions are similar so you can do something about it BEFORE it gets that ugly. My goal when I created this website was a simple one: help my fellow investors avoid a repeat of 2000 and 2008. I went out and educated myself and looked for answers...and I think I found them.